Increasing your Credit score to 800 is a difficult task but can be achieved, and today, I am going to spill all the secrets to you. But before we begin exploring these tips, you might be interested in reading our 11 Steps credit repair guide to rebuilding your credit from a bad credit score.

Let’s start with understanding the FICO scores and what they mean,

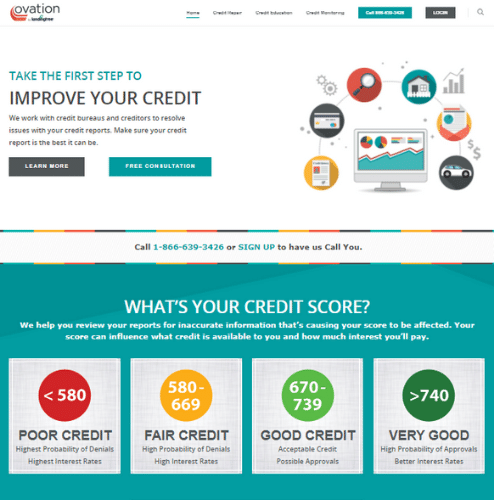

- 800-850: Exceptional

- 740-799: Very good

- 670-739: Good

- 580-669: Fair

- 300-579: Very poor

These scores are assigned by all the three credit bureaus (Equifax, Experian, TransUnion), and getting a FICO Score of 800 needs exceptionally excellent financial performance.

Though it is not an easy task, a few tips can boost your credit scores and take you to the 800 scores.

Here is my guide on how to increase Credit Score to 800,

1. Lower Debts

Lowering your debt to credit ratio is one of the important factors; as we know, credit bureaus keep track of all the entries. It turns out that lower debts to credit ratio are among the most important factors to keep a good to exceptional credit score.

What is lower debt to credit ratio?

A lower debt to credit ratio signifies lower debt repayments compared to the available credits. If you are having an available credit of $5000 on your credit card, you only spend 10-15% of the total credit and have only that particular amount to pay. Your credit score will boost to a higher level because your repayments are low.

When you maintain such a balance, up to 25% is considerable; there is a good shot of boosting your credit score to exceptional from very good.

Also, to track your credit score changes, you can try using our best credit monitoring services that will follow the score changes and update you when there is a change.

2. Low Debt to Income Ratio

Another important factor in increasing your credit score to 800 is by improving your debt to income ratio. When you have a low debt to income ratio, there is a pretty good chance of a hike in your credit score.

But first, what is a low debt to income ratio?

A lower debt to income ratio means that you have a good income and your repayments are low. You don’t spend enough and also repay on time. Having a lower debt to income ratio also qualify you for the best credit offers and gives you the best deal.

But is it hard to maintain it?

It is considered fairly difficult to maintain a low debt to income ratio because you need to stop yourself from spending more than required despite having good money in hand. But if you are planning to buy a home or go for a bigger educational loan or something, you might want to plant this technique months before; so it gets noticed.

3. Remove inaccuracies

Inaccuracies and Negative information has been a prime culprit in the wrong and lower credit score. So, if you are looking for a jump, you need to remove them.

You can use Dispute Bee software to make this a simple process; it helps you raise a dispute on the three bureaus, and the whole process is automated.

4. Reduced Spendings

If you are a shopaholic, it will always be tough for you to increase your credit score and not score 800.

Reduce your spending and show more available credits to all the three bureaus, this will eventually bring notice to their keen eyes, and you will have an increased credit score, may up to 800 (if consistent).

To reduce spending, you can do two things –

- Avoid Luxury

- Go for cheaper alternatives

Luxury and expensive items will never let you have the bigger pie on your credit score. Think about it, buy an expensive car, and ride it for days, then you no longer wish to have it and sell it. Do you think you will have a good return? No. Because the value is deprecated with every mile, you ride in that car.

Going for cheaper alternatives is a good choice because it does almost the same work but doesn’t label itself as a huge brand. You can also go for second cars that are available for much lesser prices and the same comfort.

5. Never Miss Payment Due Dates

Show your lender and banks that are their loyal customers and prove them by paying at the right time.

This will bring more confidence about getting a good credit score because your due payments are always clean, and it is a positive sign that makes a huge impact. The credit bureaus notice that you always come clean, and probably you have an excellent financial condition, you must have a good credit score and then boost your credit scores.

If you are having trouble, ask your family members and promise them to return whenever you have enough. Moreover, you can also go for a second shift or an extra job or start an online business with your skills that do not take enough time; these will all help you never miss a payment and pay on time.

6. Add yourself as an Authorised Member

This trick is not very well known by many people but can help you raise your credit score to 800 in snaps.

Add yourself as an authorized member to your family’s credit card; your credit reports are automatically backed by that credit card’s historical reports when you do so. If you are getting an authorization on your sister’s card who has a credit score of 800 and you are having a credit score of 750 and around, there is a high chance that you get to the score of 800 when you get clubbed.

This does not limit the range of credit scores, but it is always better to get authorization on higher credit scores.

7. Never go for Credit Pull

The most common mistake people usually make when they have a below-average credit score is to apply for a new credit card.

Let me make two things clear for,

- When you apply for a new credit card with a below-average credit score, get approved is highly impossible.

- If you are approved for a new credit card, it will either have a huge amount of minimum deposits or have other restrictions along with high-interest rates and fees.

In both situations, you are only hurting your credit score and financial conditions.

When you apply for a credit card when you have a below-average credit score, your bank is making a credit pull on your credit report, provided you may or may not get approval for the card.

This credit pull is visible to every other lender and, of course, to the credit bureaus, resulting in lower credit scores. So, if you are on fair credit, you will slide down to have bad credit. Though this sliding won’t be in an instant but is possible when multiple banks start requesting a credit pull on your reports, and this happens when you apply to various banks for a credit card.

On the other hand, paying high interest and high minimum deposits when you are low on credit score will pull you much down. Thinking if a new credit card will increase your score to 800 and act as a score booster is entirely wrong. You will only slide down two lower credit scores.

Final Verdict

Increasing your credit score to 800 is not impossible but only tricky and time-consuming. If people or companies ask if you want to get your credit score raised to 800 much faster and quicker, you need to avoid them, and they are just scamming. Follow the above practices should eventually help you increase your credit score.

We don’t ask for money or ask for a paid service to increase your credit score; if you get any emails or contact from our website, it is fraudulent, do not respond to it.

")