A damaged credit score and poor credit history can make your financial life jolt. But you don’t have to worry about how you will repair the credit scores. This descriptive guide will discuss 11 friendly ways to fix your credit report and boost your scores.

Stay with me till the end to get bonus tips and facts.

Get your Credit Fixed With Sky Blue Credit Repair and Boost Your Credit Score Like Never Before.

How to Fix your Credit Reports and Boost Credit Score – [11 Tested Tips from Expert]

Fixing your credit score is a time-consuming process, and you need to be dedicated and consistent. Moreover, this will guide will also change your financial life in a much positive way. So, let’s get started without wasting any minute.

1. Know your Credit Situation

The first and most pivotal step you need to do is to know your current credit situation.

Get the full copies of your credit report from all three bureaus (Experian, TransUnion, and Equifax). These will help you assess your current credit condition based on which you can take further steps.

Quick Tip: You can get your credit reports for free from the annual credit report or by calling 1-877-322-8228 once a year for Completely Free.

Other websites may send you deceptive copies of your credit reports. It is why the Federal Trade Commission (FTC) has also warned these websites to be fraudulent.

If you have already used a free credit report from the annual credit, you can also use credit tracing apps as Credit karma to know your credit report status.

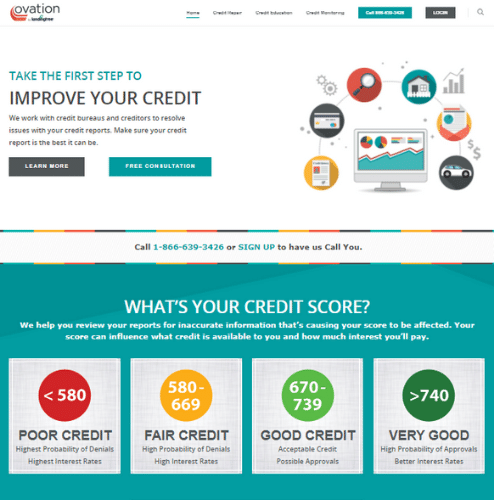

Here are the Fico Scores and want they mean on your credit report,

- 800-850: Exceptional

- 740-799: Very good

- 670-739: Good

- 580-669: Fair

- 300-579: Very poor

If you have a Fico Score between 800-739, there is a high chance of getting the lowest mortgage rates and best credit perks. On the other hand, if you are having a credit score of 669-580, you still have a chance to fix your credit report quickly and easily.

If you have a fico score between 579-300, you have a bad credit score, and you want to read this guide till the end to fix it.

The best and fast way to get your Fico Score is using the MyFICO. Get the complete credit reports, $1 million identity theft insurance, and many more perks with the premium version.

2. Dispute Error in your Credit Reports

There are no full chances that of getting an error on your credit reports. If you find any inaccuracies in the credit reports, you have all the legal rights to dispute them.

For instance, if you have a misinformed mortgage loan on your credit report, it will hurt your credit score. Removing such inconsistencies and inaccuracies will help you in boosting your credit score.

Moreover, these inaccuracies will make it hard for you to borrow money in the future, as your reports show you are in debt of a lot of money.

What to do if you find inaccuracies in your credit report; Here are the Steps –

1. Know the source:

We get a credit report or a credit history from three departments (Experian, TransUnion, and Equifax). You need to know which department is responsible for the inaccuracies and then file a complaint.

2. 609 Dispute Letter:

Now that you have figured out which department is responsible for inaccuracy, send them a 609 dispute letter from the certified mail address. This dispute cannot ensure a deletion but allows a thorough recheck by the dedicated bureaucrats.

3. Wait for the response:

Once you have sent the mail, wait for the response, this can usually take up to a month. If there are any inaccuracies in your credit report, they will be deleted and this also increases your credit score.

4. Contact:

If there is no response to your dispute, you can follow up with the bureaucrats or submit a complaint to the Consumer Financial Protection Bureau. In critical situations, you can also take the help of a consumer protection attorney.

The above steps are useful, but tracking credit reports can be hard this way. We recommend using “Credit Monitoring” services that will instantly help you know your credit changes. Moreover, this practice will also help you realize any fraudulent charges to your credit score.

Experian’s Credit works are giving free credit score monitoring; have you checked it out yet?

3. Pay the Bills

Once you have received your credit report and everything is just fine without any inaccuracies, pay your bills on time.

But before you start paying your bills, you need to make sure you have a proper budget flow.

To master your budget gaming, the first thing you need to do is analyze your past two tax returns. Look where do you spend most of your money. Try to cut down if it is entertainment, holidays, or luxury.

Once you have analyzed your tax returns, start preparing your budget for each month. You can start doing this by subtracting all the EMI options such as car mortgages, down payment for the home, and health insurance.

Then I want you to estimate the amount of money you spend every month. It can be about groceries, entertainment, holidays, luxury, or pleasure.

Now, cut off or minimize all the unnecessary expenses and create a limit for each of your spending habits. This way, you can spare a bit extra each month to help you pay your credit debts.

Additionally, I want you to stop adding extra credits to your credit card. You are already in debt, and adding more will only hurt your credit score. Instead, try minimizing your needs or go for a cheaper version, and this way, you will not load more on your credit score.

4. Paying on Time is the Ultimate Factor

Paying your bills on time is the ultimate factor for credit repair. If you keep monthly dues and do not pay on time, you won’t be able to fix your credit score.

Check your credit reports and make a list of pending dues to pay them off as quickly as possible. On the other hand, paying your dues on time will also reduce the interest rates and boost your credit score.

But wait, how you don’t get bills for services such as monthly phones and utilities? Let Experian do that for you. Experian Boost links with your bank for such small transactions and keeps an eye on unpaid dues.

Best part? Experian boosts this for free, and on average, users have reported up to 15 points increase in their Fico score once they start using the Experian boost.

5. Set the Right Credit Limit

Your credit card limit is one of the most important factors that credit bureaus consider while analyzing your credit report.

This is because the credit bureaus calculate your credit reports in ratios. Let’s see this with an example.

Suppose your credit card limit is $1500, and you only spend $500 in the month. When you calculate the ratio, the percentage roughly falls to 33% which is great for your credit report.

Calculation: (500/1500)x100 = 33.33%

On the other hand, if your credit card limit is $1000 and you spend the same amount($500), you are spending over 50% of your credit card; this can make a negative impact on your credit report.

Calculation: (500/1000)x100 = 50%

The best practice is to know your expenditure and set the right limit on your credit card. Doing so will make a good impact on your credit score.

6. Don’t Apply for a New Credit Card

Applying for a new credit card is a bad option though the banks give you exciting offers. Having a due on your credit score and applying for a new credit card negatively impacts your credit score.

If you have a below-average credit score and apply for a new credit card a few times in a year; your application is treated under hard inquiry. This results in a decline in your credit score.

Consumers with a good credit score can apply for a new credit card a few times in a year before it starts negatively impacting them. It is wise not to trap yourself in new exciting offers that you don’t need.

7. Cut-off Luxury

Luxury is tempting but will only take more and more from you. Get cheaper versions of products for you that works the way luxury products do.

If you are running on a fair or average Fico score, you need to minimize or remove luxury from your credit. What you can do instead is look for a cheaper alternative that works in the same fashion.

8. Do not Buy a New Car

Buying a new car when you have a low credit score is a bad option. If you plan to buy a car, do not buy a new car; instead, go for a second-hand car.

Let me explain to you the reason,

When you try to sell your new car, you get less than or equal to half of the original price. But when you buy a second-hand value of the same car, you will spend less on your credit for the same performance.

Buying luxury with small hacks will help you not overspend on your credit. On the other hand, you also need to pay your dues on the due dates.

9. Do Not Go for Down Payments / EMI options

Down payments and EMI options are what you need to avoid. When you are running on a low credit score, going for down payments and EMI options will only hurt your metrics.

Bureaus will notice them as unpaid dues and decline your credit score. The best you can do is patiently wait until you have saved enough to buy the product or services. This way, there won’t be any unpaid dues on your credit report.

10. Get Yourself Added as an Authorized user

A lot of people don’t know about this simple hack that helps you rebuild your credit score.

If you have a friend or family member with a credit card, ask them to add you as an authorized user. This way, their credit history is clubbed with yours, and your credit score boosts overall.

Note: The person you are clubbing your credit with should have a great credit score to boost your credit score overall.

11. Do Not Pay For Disputes When You Are Sure

When you are sure about having a dispute on your credit report and have submitted it for a review to dedicated bureaus, do not pay until the confusion is clear.

It takes up to one month for bureaus to cross-verify your disputes. You can raise a dispute and track it using Dispute Bee credit repair software.

Final Words

Rebuilding your credit score is not that difficult. All it needs is a few adjustments and awareness on how you should properly use your credit card.

The first and foremost thing you need to do is know your credit situation and raise disputes when you find inaccuracies.

Always pay your bills on due dates, and do not pay for disputes when you are not sure. If your credit disputes are still not verified, you can take the help of a credit attorney.

Frequently Asked Questions

You can repair the credit score on your own when you don’t have negative credit information.

Legitimate credit repair companies help you boost your credit score by removing inaccurate credit entries. Beware of scamming credit companies that assure to boost your credit score and demand money.

The 609 dispute letter is a method of requesting the removal of any inaccurate negative information from your credit report that can hurt your credit score.

The only way to remove the negative entry from your credit report, raise a dispute, and send a letter to a dedicated bureau for a thorough recheck.

")